💸📆A 10-minute guide to budgeting

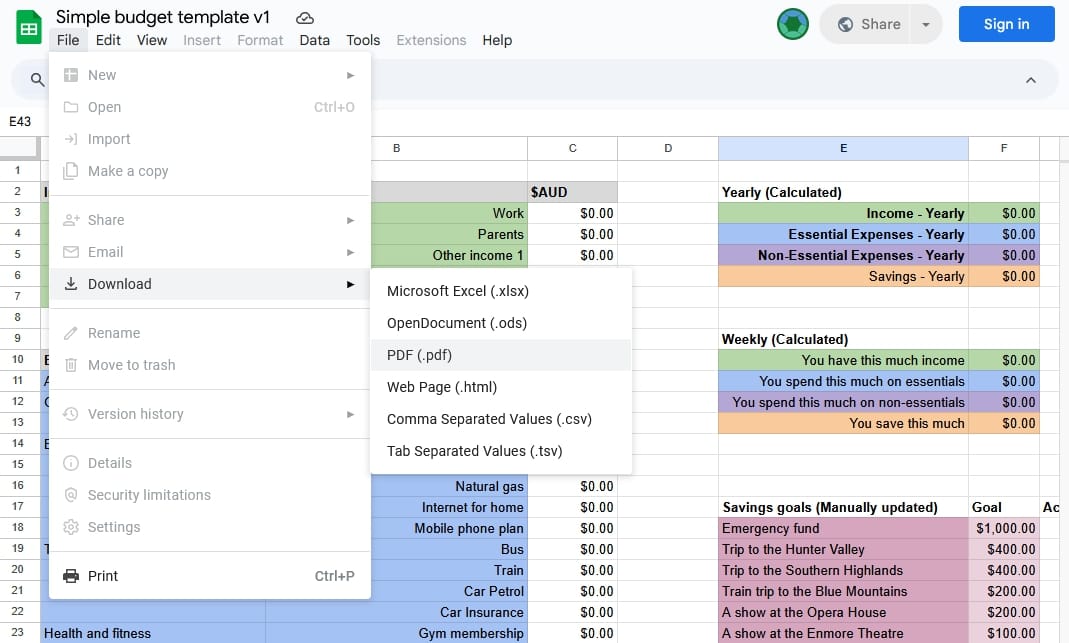

Stressing about money and can't be bothered to learn? Here's a quick guide on how to budget your money while studying in Australia. You can download this template and use it as a guide for the rest of the article.

中文版

हिंदी संस्करण

Stressing about money and can't be bothered to learn? Here's a quick guide on how to budget your money while studying in Australia. You can view and download this template and use it as a guide for the rest of the article (start with the simple template, although the complex version is easier to track over time, see the bonus step at the end of the article to understand why).

Four steps to budgeting (plus a bonus step)

- Track your basic income and expenses.

- Save money towards an emergency fund.

- Give yourself spending money.

- Create saving goals.

- [Bonus] Gain greater control over your finances.

Track your basic income and expenses

Most people usually don't have too many sources of income. However, we often have expenses that we don't remember until it appears in our bank account records. Tracking both allows you to more intentionally decide where you would like to spend or save your money.

Save money towards a rainy day / emergency fund

A rainy day / emergency fund could be used for a variety of purposes, including medical, accommodation (eg. eviction) and travel emergencies, so it would help to have $1000+ in a savings account that you can draw on when needed. While this won't cover all possible emergencies (that's what health and travel insurance is for), it will add to your peace of mind knowing you have access to money immediately instead of having to ask your parents overseas or borrow money with high interest.

Give yourself spending money

This refers to fixing your non-essential spending money to a reasonable amount within your means (ie. less than your income minus essential expenses). Giving yourself spending money allows you to psychologically set boundaries and expectations for your own habits. This way, when you encounter something you want to buy, it's much easier to decide yes or no because you know how much you can spend. The worst situation to avoid is when you want something and you don't know the consequences of your spending (eg. spending money from a credit card on impulse purchases).

Create savings goals

Now that you've tracked your income and expenses, set aside money for emergencies and set a fixed amount for your non-essentials, you're feeling pretty good about yourself 😇. It's time for savings goals!

Saving goals is a great way to set money aside for longer term spending goals you may have. The budget template has some suggested saving goals and estimated amounts (eg. trip to Hunter Valley, watch a show at the Opera House). As long as you can commit to not touching that money until you use it for that specific goal, you'll be able to enjoy your time in Australia without ever worrying about spending too much!

[Bonus] Gain greater control over your finances

If you want greater control over your finances, you can also track your income, expenses and savings week-to-week in the complex version of the budget template. Here's a few tips for using the complex version:

- Start by setting a rough yearly goal for each line item in income, expenses and savings. This should take you 30-60 minutes, depending on how much experience you have with Australian living costs. Don't be afraid to search online for prices of household goods or travel packages. Doing this one can save you so much time later on.

- It shouldn't take you more than 15 minutes per week to track everything you've spent or earned. Just fill out one vertical column per week.

- The cells with a coloured background are calculated cells (ie. don't touch them). Only fill in the cells with a white background and slightly grey text (I made it grey to make it easier on your eyes).

- Row 57 "Savings" with an orange background should tell you how much you are saving in every week / column. This savings total should then be distributed to the orange cells below in your savings goals. In other words, every week you:

- Receive money

- Then spend a portion on essentials

- Then spend a portion on non-essentials

- Don't forget to put a little under "Cash you carry"

- Then whatever money you have left over is your savings

- Then split up your savings into your savings goals

- This is a manual process, the spreadsheet doesn't do it for you, sorry 😅

- Then whenever you hit your savings goal you're ready to spend it!

Happy budgeting!